Although the year-over-2018 revenue of wide-format printing service providers (PSPs), was lower in 2021 than expected, most PSPs felt moderately optimistic about an economic recovery. Photo courtesy Media Resources Inc.

Eve Padula and Eric Zimmerman

Since the COVID-19 pandemic, more than two decades have passed. The dramatic changes that have happened since then are unprecedented. These changes were certainly felt in the wide-format print industry. Graphic communications and signage are essential parts of society. Many wide-format printer service providers (PSPs), were able pivot their applications to weather the storm.

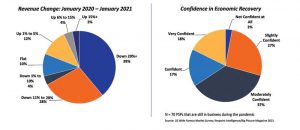

While revenue volumes for 2021 were lower year-over-year, PSPs are optimistic about the near-term recovery.

PSPs were less cautious about purchasing equipment in 2021 because volumes were lower than they were before the pandemic. Nearly two-thirds (64%%) of PSPs didn’t plan to purchase new equipment in the early 2021. There has been some improvement in wide-format printing sales since that time.

Wide-format applications were stable despite the disruptions caused by the COVID-19 pandemic. Signs, banners and stickers were the most popular products in high demand when PSPs were asked. Floor graphics were also in high demand during the heights of the pandemic.

The industry of wide-format printing will see continued recovery as we move into 2022. Supply chain disruptions, labour shortfalls, and concerns over COVID-19 variants all will continue to be challenges even as demand grows. This article presents a forecast overview and examines wide-format growth areas likely to assist the industry in regaining lost volumes in 2022.

Figure 1 – Year-over-year revenue change and confidence in economic recovery.

Forecast for ink technology

According to Keypoint Intelligence’s (KPI’s) most recent forecast data, placements of all wide- format technologies are expected to remain generally flat between 2019 and 2025. This flatness can be seen as a recovery due to the sharp decline in printer placements across all ink technologies from 2019 to 2020. As we move through the current forecast period, all technologies are expected to continue recovering.

Important to note that this forecast data would usually cover a five year compound annual growth (CAGR) between 2020-2025. To measure the rate at which recovery is occurring, it is crucial to establish a benchmark pre-COVID. KPI will use a six year CAGR (2019-2025), to give a realistic and clear view of the market.

Aqueous

After performing below forecast in 2019, and being faced with the pandemic, the wide-format aqueous ink printer category experienced a 25% decline in unit sales between 2020 and 2019. Year-over year, the biggest decline was in production (38%) and a 27% drop of print volumes. The creative segment suffered the smallest year-over-year decline in unit sales (12%) As a result, the category is expected to see a quicker recovery in 2025.

The overall segment is making progress, but it is likely that it will still take some time for it to reach pre-pandemic placement levels.